I was speaking to Ravi who has significant investments in real-estate. Ravi owns several properties that he rents out. Ravi said that his investments in real-estate are like investments in equity. He said that investments in real-estate like equities have 2 sources of value

- Rent – which is like dividends from equities

- Capital appreciation of the property is like the price appreciation of a stock.

I think this is a popular misconception. I believe real-estate can be best compared with bonds than equities. Let’s look at real-estate, bonds, and equities along a few dimensions:

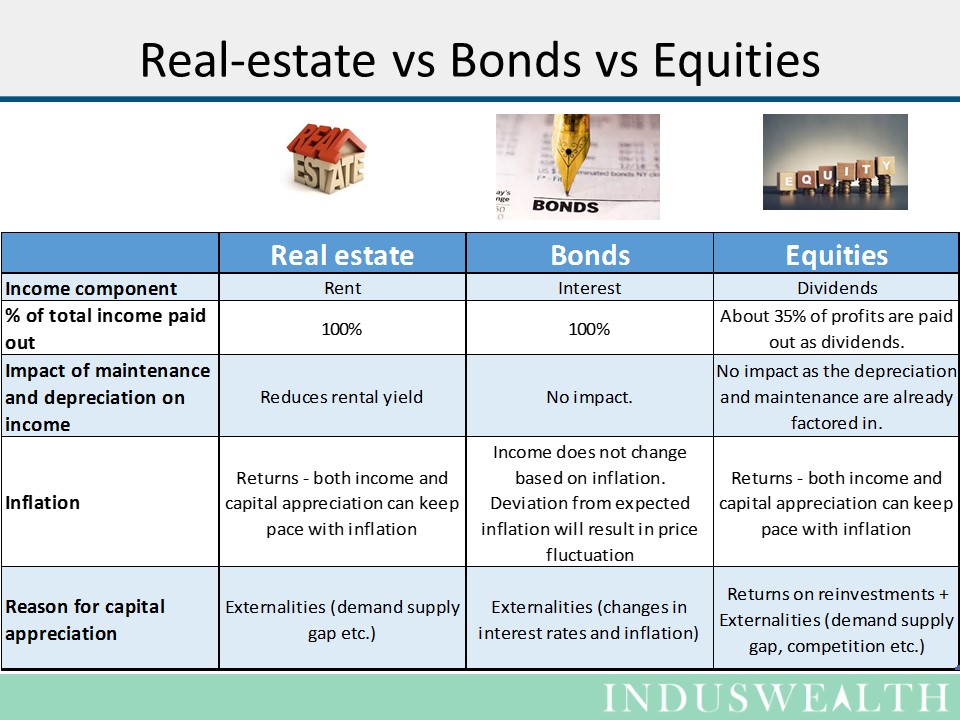

% of income paid out:

- Real-estate generates income as rent and all of it is paid to the owner. Rental yields (rent/current price of property) are typically in the range of 2% (residential) to 7% (commercial).

- Bonds pay out all the interest received to the bond holders. Bond yields (interest paid/current price of the bond) are typically 7% (blue chip) to 14% (higher default risk).

- Equities pay out a part of the profits as dividends. Dividend paid by a company is typically 35% of its earnings. Rest of the earnings are retained for future investments. Dividend yields (dividend per share/current price of stock) are typically 1.2% to 2.5%.

Maintenance and depreciation:

- Real-estate owner must pay for the maintenance and depreciation from the rental income. This reduces rental yield.

- Bonds don’t have any maintenance or depreciation component.

- Earnings per share (EPS) is calculated after factoring in the depreciation – i.e., any maintenance and replacement required is already factored in.

Inflation:

- Real-estate rentals and prices typically tend to keep pace with inflation. Owners can typically increase rents to keep pace with inflation. Also, the prices of the property can increase in line with inflation assuming there is no significant change in the demand supply situation – i.e., the percentage of wealth a person will be ready to pay for a property may remain constant.

- Bonds typically factor in the expected inflation in their interest rates but if there is a significant change then it cannot be dynamically accommodated by the bond. Bond prices will appreciate if actual inflation is less than the anticipated inflation and vice versa.

- Usually businesses can successfully pass on increase in costs to their customers so their returns typically keep pace with inflation. Overall prices of stocks can also keep pace with inflation as the percentage of wealth a person will be ready to pay for a business may also remain constant.

Capital appreciation/depreciation:

- Real-estate appreciation can be due to 2 factors a) demand supply gap and b) inflation. Demand supply gap can be due to laws or geography limiting the amount of supply available (London, New York, Mumbai etc). It could also be due to the changes in the economics of the property location – for instance factors like proximity to industry or if there is a new project (rail road or a park) that affects the demand supply. Each of these could have a positive or a negative effect – for example, job creation by industry can increase the value, pollution could decrease the value. Real-estate values tend to keep pace with inflation. Real-estate price appreciation is based on changes in demand supply, inflation and other external factors hence the owner has no influence on its capital appreciation. Appreciation/depreciation which is higher than the inflation rate can be largely attributable to chance.

- Bond prices fluctuate due to changes in interest rates. If there is a fall in the interest rates than the bond price will appreciate as vice versa.

- Equity represents ownership of business and if the business can reinvest retained earnings to generate future income then its value increases. Investing of retained earnings is like an apartment owner adding new apartments from the rentals to generate more rental income. This ability to generate additional future income creates price appreciation component that is unique to equities. Equity prices can also change due to changes in demand supply of products that company manufactures, change in competitive landscape etc. Brands or patents that give sustainable pricing advantage can lead to increase in price of the stock, increase in competition or poor management can reduce the price of the stock. Equities prices tend to keep pace with inflation. Equity price appreciation/depreciation has a component that is not dependent on chance and hence it is reasonable for equity owners to expect price appreciation that is greater than the inflation rate.

In summary

- Income: In terms of income bonds give a better income than both real-estate and equities. Rental yield of equity is typically higher than the dividend yield from equity, but after factoring in maintenance and depreciation the difference may not be significant.

- Inflation: Bond income (interest) does not keep pace with inflation, whereas rental yields and dividends typically tend to keep pace with inflation. Bond prices go down with increase in inflation and up with a decrease. Whereas real-estate and equity prices typically tend to keep pace with inflation therefore investors can expect inflation adjusted returns.

- Capital appreciation: Bonds and real-estate are dependent on externalities for capital appreciation. Appreciation/depreciation which is higher than the inflation rate can be largely attributable to chance. Equities price fluctuation has 2 components – reinvestments and externalities. Appreciation due to reinvestment is not dependent on chance and hence it is reasonable for equity owners to expect price appreciation that is higher than the inflation rate.

I hope this discussion gives a framework for looking at returns from income and capital appreciation from bonds, real-estate, and equities.

Happy Investing….