Every product we buy comes with a user guide, this is not the case for services. We thought we should create a user guide to assist our clients to make the best use of our services.

We felt it is best to start off with “Don’ts”, then go on to the “Do’s”, then follow it up by how it works and what you can expect, and finally how to review our performance.

Don’ts

- Invest in equities if you are convinced that they are the best products to create long term wealth. If you are not convinced then equities are not suitable for you.

- Equities are best for people with a long term horizon, at least 5 years, preferably 10. If your investment horizon is less than 5 years then equities are not suitable for you

- Equities are inherently volatile, be prepared for to ignore the volatility. If you are uncomfortable with volatility or unable to ignore it then equities are not suitable for you

- Once in a while there will be significant corrections in the market, and that may not be the time to exit, it could be a good time to buy. If you find dealing with significant corrections uncomfortable then equities are not suitable for you

- Your ability to withstand volatility is more important than your willingness to do so – if you may need to withdraw the funds invested in equities, especially when there is a crash then equities are not suitable for you

- At IndusWealth we believe that predicting the market is not possible, we are taking a systematic approach to investing, we believe it gives the best opportunity to make a reasonable return. If you are keen on market timing and plan to invest only when you believe that markets will do well – then IndusWealth services are not suitable for you

- At IndusWealth we are trying to build your portfolio over 36 to 60 months, if you are unable to invest regularly (monthly) – then IndusWealth services are not suitable for you

Do’s

- Invest regularly as a general practice, you should consider directing a part of your investments into equities.

- It is advisable to have at least 30% of your net worth in equities, you should try and build this position over a 3 to 5 year period by investing regularly

- Review your portfolio on a regular basis, we suggest quarterly – it is important that you stay informed (we also suggest that you should avoid looking your portfolio more than once a month)

- Please review your portfolio with us once a year

- Please discuss with us if there is a significant change in your goals or financial outlook

- Please sound us out on any large investment you are planning to make. We don’t claim expertise in many areas but we can be a good sounding board and can give you a list of questions that you should be asking before making that investment.

How does it work (investing rationale) & what should you expect

We are taking an analytical, incremental, and disciplined approach to investing. There are always going to be trade-offs between opportunity to make a profit vs a chance of losing capital. Our approach is to be ok with missing out on opportunities and make the best attempt to preserve capital. The underlying belief here is that capital is limited but opportunities are not.

- You will see investments being made in 4 to 6 stocks every month. These investments are made in the first 2 business days of the month (usually first business day, sometimes second).

- If you are investing over a 2 year period, your portfolio can be expected to have more than 40 stocks. This is a natural outcome of the overall approach.

- You should expect about 80% of your funds to be invested in about 40 stocks, also expect to see a bit of “long tail” (small investments made in multiple stocks) as we try and explore opportunities in the market.

Buying:

- A stock is purchased when, based on our analysis, there is a chance of 20% or more upside in the next 12 to 24 months. Chance does not mean certainty, sometimes this does not happen. It could be that the analysis was incorrect or it may take longer for the upside to materialize.

- We will try and reinvest in a particular stock as long as the expected 20% upside is available. There is a conscious attempt to avoid investing too fast into a particular stock, that is the reason you will see that reinvestment in a stock is done only after a quarter has passed from the previous investment. We expect good stocks to have a long period of growth. We are trying to avoid errors in our analysis leading to a large investments that are not prudent. We are also trying to avoid short term trends in the market that lead to permanent capital loss.

Selling: Cases when a stock is exited

- A stock purchased that has not given the expected return over 18 months. Based on our analysis there was a potential 20% upside which has not materialized, this could mean our analysis is incorrect or it could take longer to realize the upside. We exit because there could be other opportunities that can be pursued with the funds than to stay invested.

- The stock is being currently held but the analysis does not justify further investment, as it may not have the 20% upside that is required to make an investment. The way we see it, holding a stock is same has choosing to invest in that stock. As stocks can be easily converted to cash, holding a stock on a particular day is equivalent to investing that amount in the stock on that day. Our approach is:

- Stocks that don’t offer expected upside are categorized as “rationalize”. It is possible to have more than one stock in the rationalize category.

- Based on our analysis, these are ranked and exit starts from the one that is deemed least desirable and we work up the chain in a gradual manner.

- Sometimes when there is a large position (more than 1% of the total holdings), there can be a partial exit. The attempt here is avoid a possibility that our analysis may not be right and the stock could still have upside. The attempt is to not rush into big decisions fast that way even if errors are made they are small.

Performance appraisal

Our objective is to beat the market (NIFTY) in the long run. Out target is to build your portfolio over 36 to 60 months. You will have reasonably representative portfolio after making 18 to 24 monthly investments. 18 months is a reasonable time frame for you to have a serious review of your investments. You should expect some of the investments to do better than NIFTY and some to do worse.

Reviewing your portfolio performance

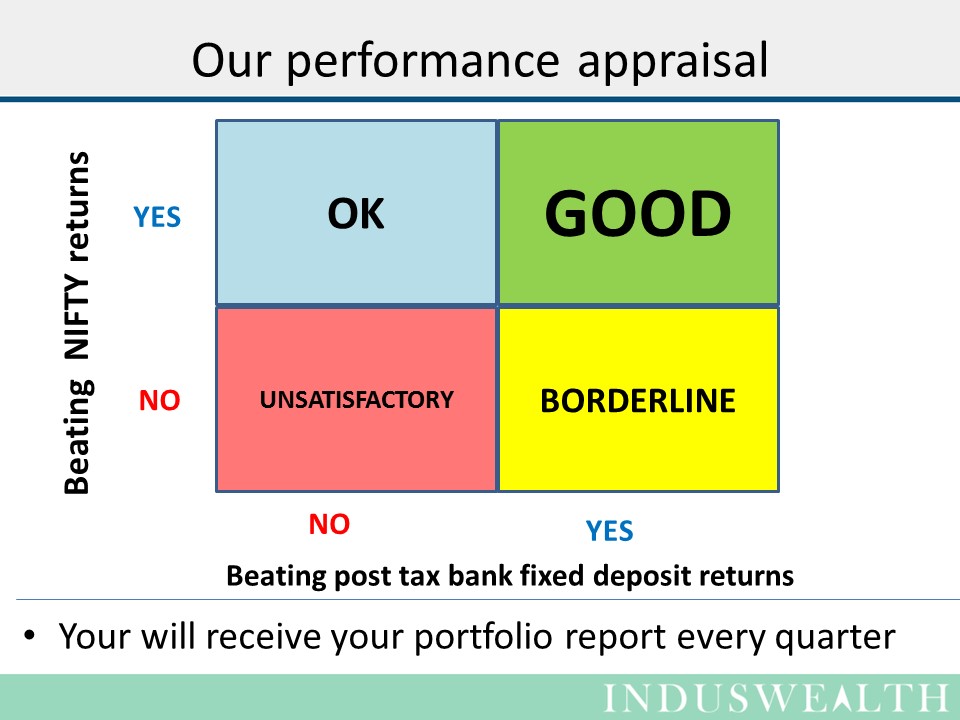

Our investment objective is to genereate alpha. We use two benchmarks to review the portfolio performance 1) post-tax bank fixed deposit rate and 2) NIFTY. Equity investments are best assessed with market as the benchmark. You should consider your portfolio performance to be ok as long as it is beating NIFTY return, even if the portfolio and NIFTY does not beat the bank rate. Here is how we would categorize performance:

- Unsatisfactory: If your portfolio is losing to bank return and NIFTY return after investing for 18 to 24 months.

- Borderline: If your portfolio is beating the bank return but losing to NIFTY return after investing for 18 to 24 months.

- OK: If your portfolio is beating NIFTY returns but losing to bank return after 18 to 24 months, you should consider continuing as markets in the long run have generated better returns than the bank rate. Please remember fees will not be assessed till your portfolio returns exceed post tax bank fixed deposit return.

- Good: If your portfolio is beating NIFTY return and bank return after 18 to 24 months then, we believe, you are getting reasonable return on your investment.

This is an attempt to assist you to best utilize our services and evaluate our services. Please reach out to us for any questions.

Happy investing …

![]()

IndusWealth Advisors, is a SEBI registered Investment Adviser – registration number INA200016856

IndusWealth:Making your money work for you