Parents and prospective parents intuitively understand the importance of college education and are keen to ensure that they have enough funds to support their kids through college.

Common challenges in planning for college are

- Starting too late

- Saving too little

- Selecting inappropriate products

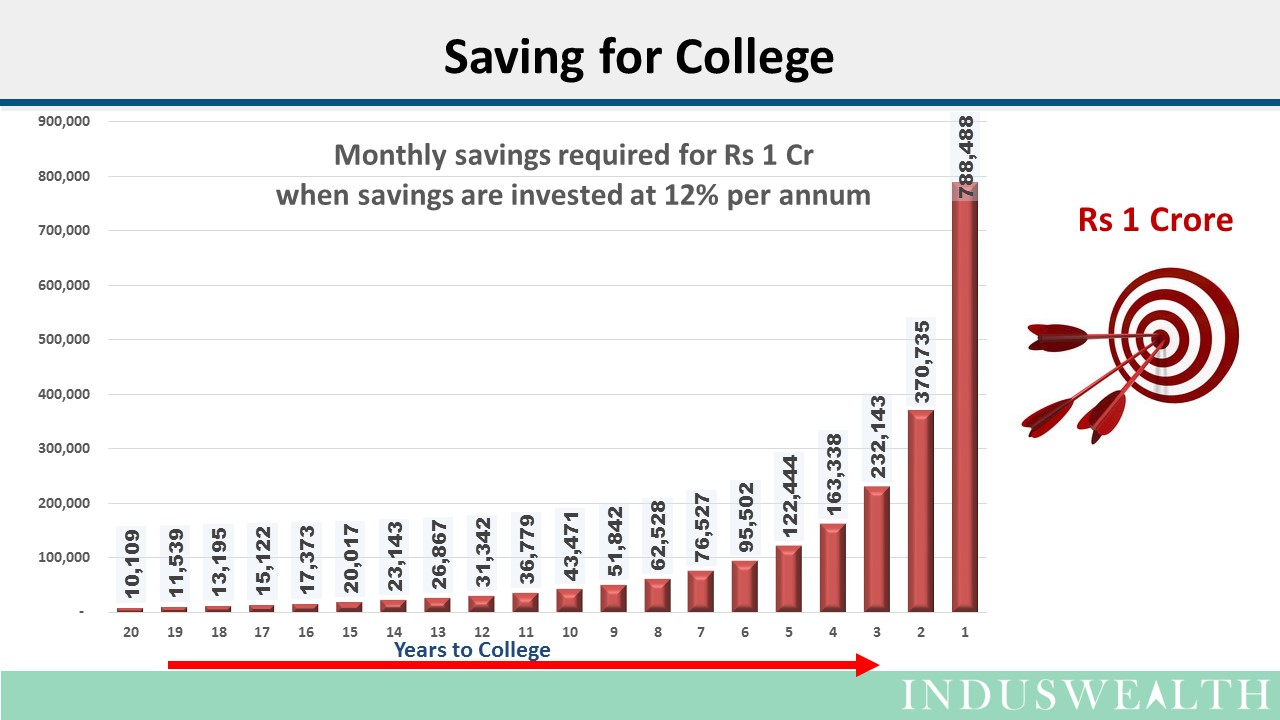

Starting too late: Saving for college becomes a must once the child is born. When the child is born, college seems too far away and saving for college may not be a top of the list item. But one needs to realize that the later one starts the more one has to save. Let’s say Anitha’s parents want to save Rs 1 crore for her college which is 17 years away, they need to invest Rs 15,000 a month for the next 17 years. If they delay investing for 2 years, i.e., when college is 15 years away, they need to invest Rs 20,000 a month. If the college is 10 years away they need to invest Rs 43,500 a month. Pl note in this example we are assuming a 12% rate of return on investments.

Saving too little: Most parents are keen to save and do put away some money, but the magnitude of savings is very important. If one is putting away amounts smaller than that is required to fund the education, one may have a significant shortfall. If you would like to understand more about identifying a savings target that is relevant for you, click here to read an article we published earlier.

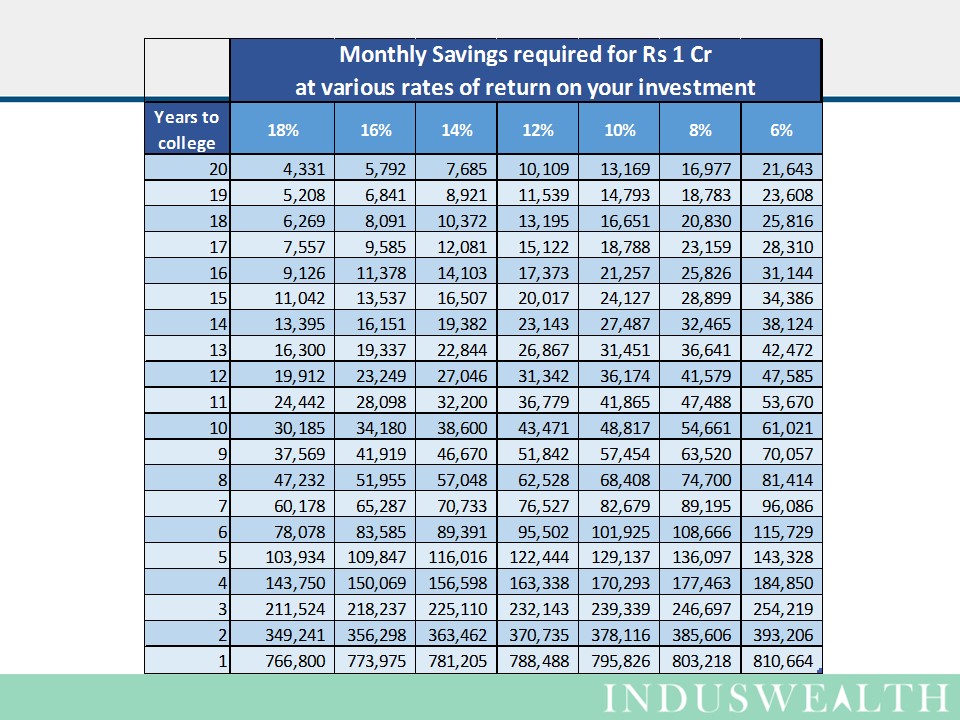

Selecting inappropriate products: Planning for college is usually a long term goal, selecting the right product is key to meeting this goal. Long term rate of return of the products you invest in will have a significant bearing on the magnitude of investments. Also please remember to take taxes into consideration as returns on many products will be taxed, thus reducing their realized rate of return. Let’s say Anitha will go to college after 17 years. If Anitha’s parents choose to fund her education by investing in bank fixed deposits that give 8% – they need to be investing 17,000 a month. Bank fixed deposits are taxable (say 25% tax) so their effective return is only 6%, then they should be investing 21,500 a month. If they are investing in Index ETF’s that have a long term return of 14%, they need to be saving Rs 7,700 a month. ETF returns are also helped by the fact that there is no tax for holding equities over 12 months. If Anitha’s parents are able to invest in products that generate a much higher return, say 18% post tax, then they need to be investing only Rs 4,500 a month.

We believe that equities are a great products for investing in goals that are more than 5 years away. The returns being tax free is also a big plus. We advise our clients to assume a 12% return, so that there is a bit of cushion. This will also enable them to slow down their investing in the future if they are well ahead of their planned targets.

Sending your kid to college could be one of the best investments you can make for your kid. Investing your savings smartly will enable you to do that.

Happy investing……