Skip to content

Home

About Us

Our Purpose

Letter to investors

India’s Investment Story

Registration Info

Our Services

Our Proposition

User Guide

Compliance

Blogs

Our Publications

Menu

Home

About Us

Our Purpose

Letter to investors

India’s Investment Story

Registration Info

Our Services

Our Proposition

User Guide

Compliance

Blogs

Our Publications

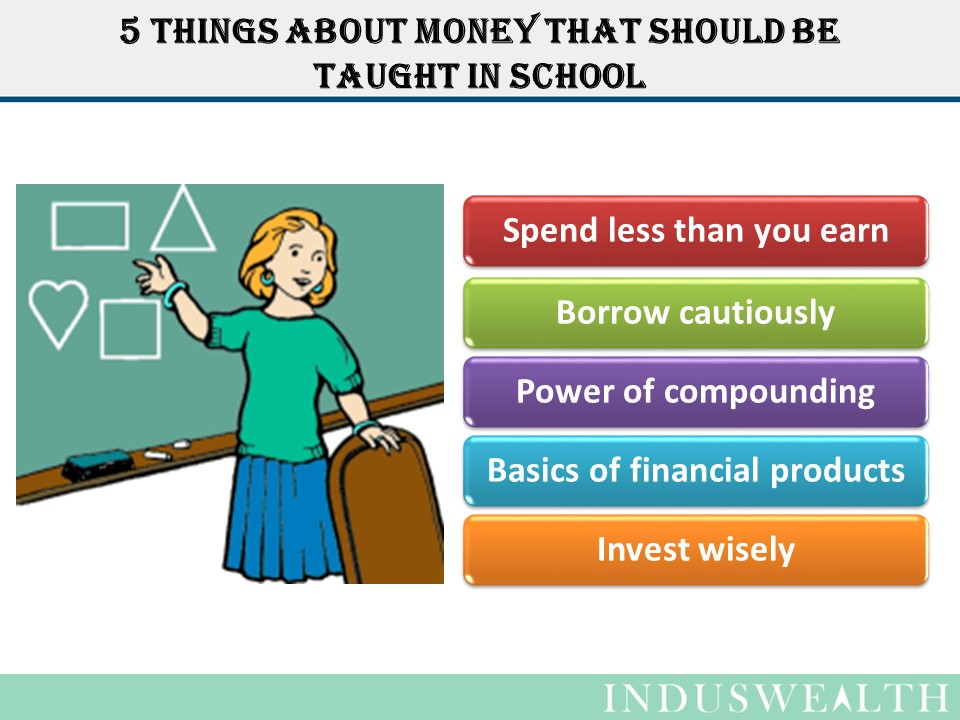

5 things about money that should be taught in school

5 things about money that should be taught in school