Uncertainty has become the norm rather than the exception in today’s global environment.

The Russia–Ukraine conflict has now stretched over three years. Tariffs and trade realignments among major powers — the US, China, and Europe — are reshaping global supply chains. The ongoing Middle East conflict has constrained traditional energy supply, creating short- to medium-term inflationary pressure. Layered on top of all this, the rapid development of AI and the capital expenditure it demands present both fresh opportunities and new disruptions.

In this era of persistent uncertainty, investors must assess the implications for portfolios across short, medium, and long time horizons. Here is a structured view of the current landscape:

Macro risks:

- Energy supply constraints (oil, fertilizers, and oil derivatives) are likely to sustain inflationary pressure globally, with supply chain disruptions persisting in the short to medium term.

- AI investments are creating meaningful tailwinds for infrastructure providers — data centre builders, electricity generators and distributors, and hardware suppliers — while posing headwinds for roles that AI can perform faster and more cheaply.

- The Indian rupee faces continued depreciation pressure in the near term. FII outflows from Indian equities have been at historically elevated levels — with net outflows hitting a record Rs 1.58 lakh crore in 2025, the largest since FIIs began investing in India. These outflows are partly self-reinforcing: FII selling weakens the rupee, which in turn incentivizes further FII exit.

Connecting macro to investing:

In the oil market, the current structure — where near-term spot prices (above $110) trade at a meaningful premium to forward contracts (about $85 for December 2026 contacts) — signals that markets anticipate a reduction in geopolitical risk over the coming months. While markets are imperfect forecasters, the weight of real capital behind futures prices makes this a meaningful data point.

Indian corporate balance sheets are in a relatively healthy position: leverage has declined, asset utilisation is high, and the banking system is primed for a fresh credit and investment cycle. The drag has been subdued private investment, which remains the key variable to watch.

India’s structural growth story — demographics, formalization, digital infrastructure — remains intact. The risks are execution-related: persistent inflation, the pace of regulatory reform, and the government’s willingness to reduce bureaucratic friction (what might be called “regulatory cholesterol” — the accumulation of rules that slow business activity without adding proportionate value).

Valuation perspective:

On fundamentals, the Nifty 50 P/E currently stands at approximately 20x — below the long-term historical average of ~23.5x (2009–2025). This suggests the market is not expensive on a historical basis; in fact, it offers a modest valuation discount relative to the mean.

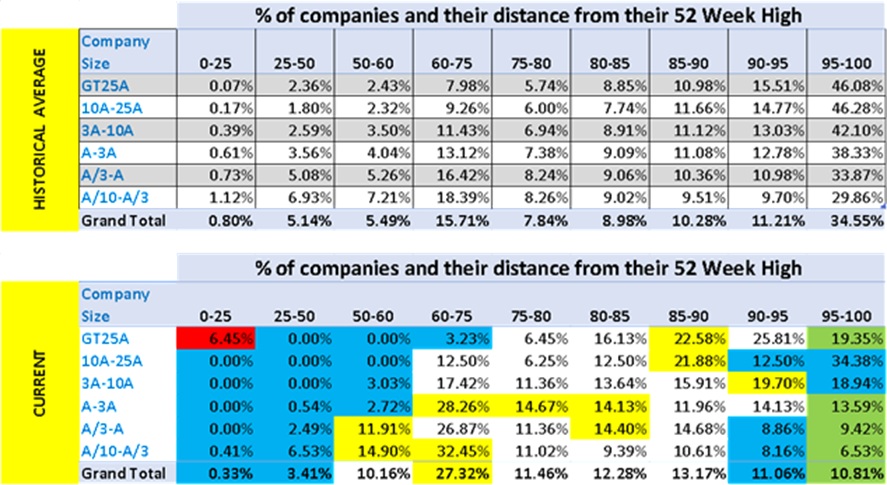

On the technical side, we analyzed the historical distribution of stock prices relative to their 52-week highs across listed companies. We classified companies using a relative market capitalization metric: “A” represents the average market cap of the top 85% of listed companies by size in a given year. Companies were then grouped into buckets — A to 3A, 3A to 10A, above 25A, and so on — and their current price was expressed as a percentage of the 52-week high.

For the largest companies (above 25A), 46% currently trade between 95–100% of their 52-week high, and 15.5% between 90–95%. When compared against historical norms, large-cap stocks appear to have a 7–10% upside potential on a mean-reversion basis. Smaller-cap companies show even greater potential upside, making them particularly attractive for patient, long-horizon investors.

Conclusion:

Current market prices reflect substantial embedded uncertainty — which is precisely where long-term opportunity resides. The path will not be linear; any escalation in geopolitical conflicts could delay the timeline for recovery. Historically, the best investment returns have been generated by those who committed capital during periods of maximum uncertainty.

To invest effectively in such an environment, three things are required: a belief in statistical mean reversion, an optimistic long-term outlook, and the psychological resilience to endure short-term pain in pursuit of long-term gain.