All of us intuitively understand that if we borrow to purchase something we are paying more than if we paid fully up front, but we may not look into the actual numbers. This article is an attempt to present a case to do so.

When we borrow, we have the convenience of enjoying something we cannot afford today. For this we are pay an interest on the money we borrow. This can also be looked at as premium we are paying to enjoy something today.

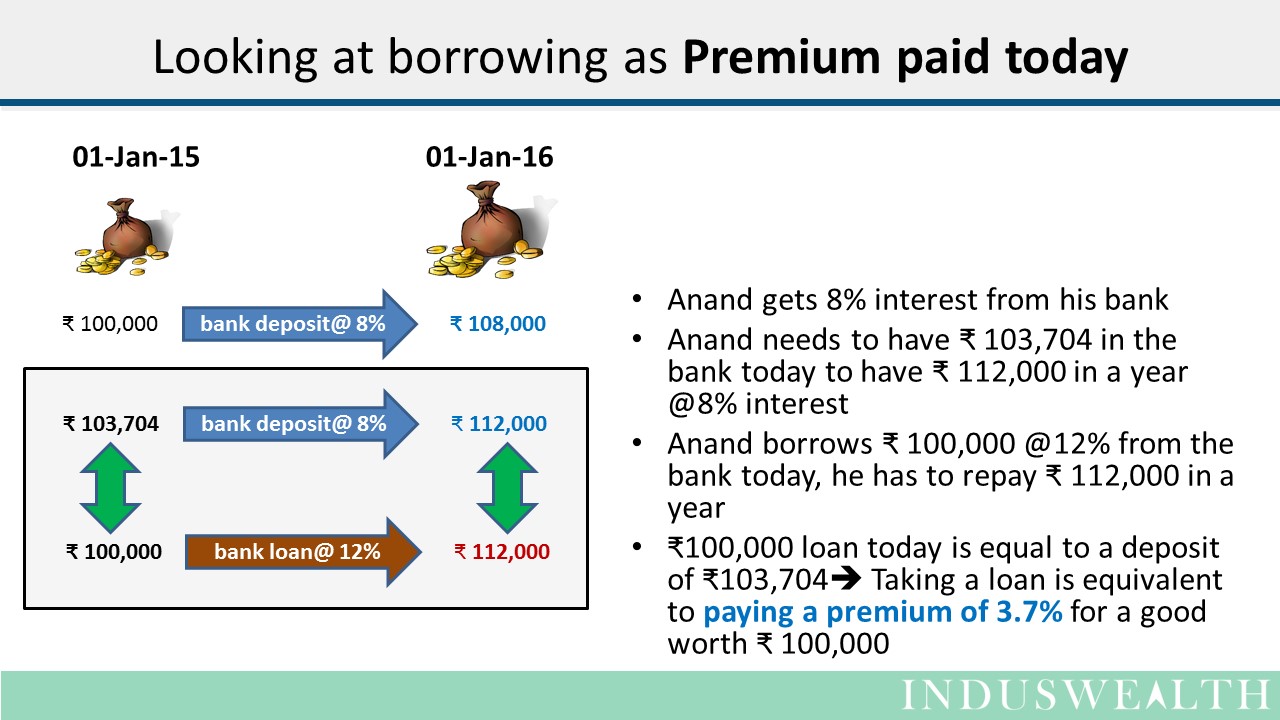

Let’s say Anand has ₹ 100,000 (1 Lakh) with him today. If he puts it in a bank fixed deposit at 8% interest, he will have ₹ 108,000 at the end of the year. This is his opportunity cost. If he consumes this today he is forgoing the interest he will receive on that money.

Based on the example, when Anand borrows @12% to buy something worth ₹ 100,000 that is same as him paying ₹ 103,704 today to purchase the good. It is a 3.7% premium for the good (when his opportunity cost is 8%). The cost of the ₹ 1 lakh loan for Anand is ₹3,704.

We can look at all loans as the premium paid to enjoy something today.

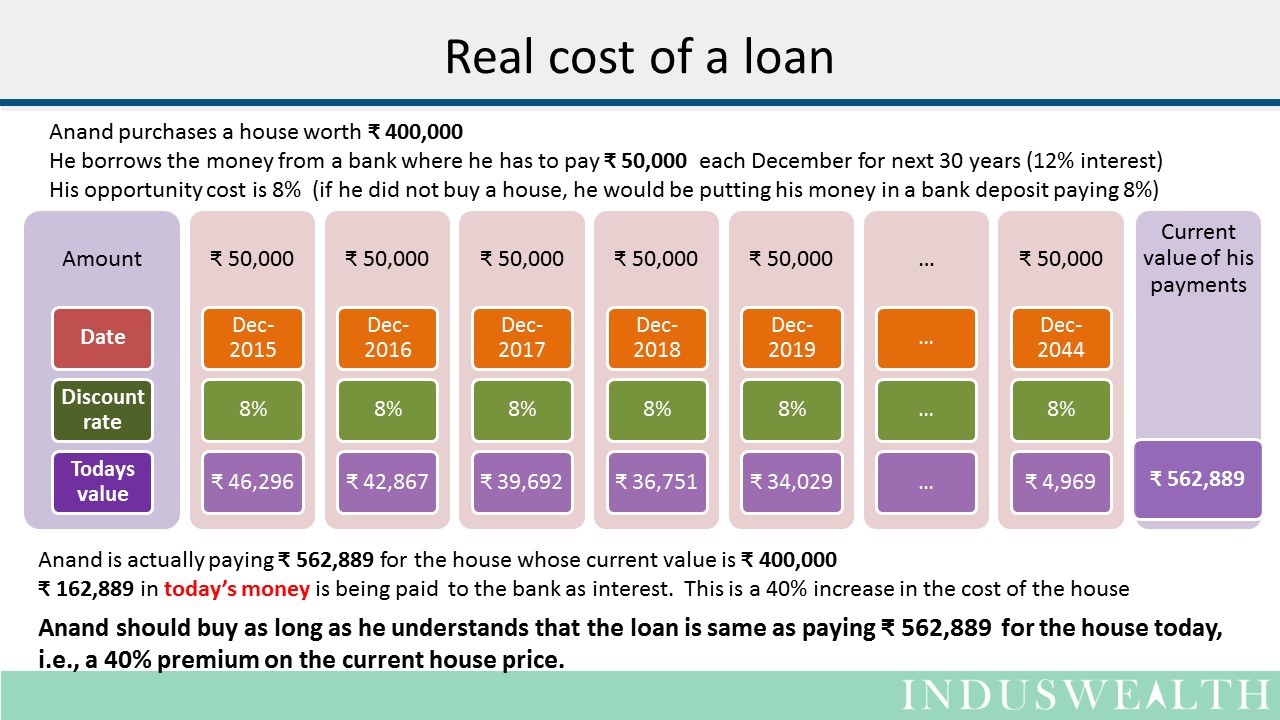

Let’s look at an example, a simplified version of the home loan before we look at real-life examples:

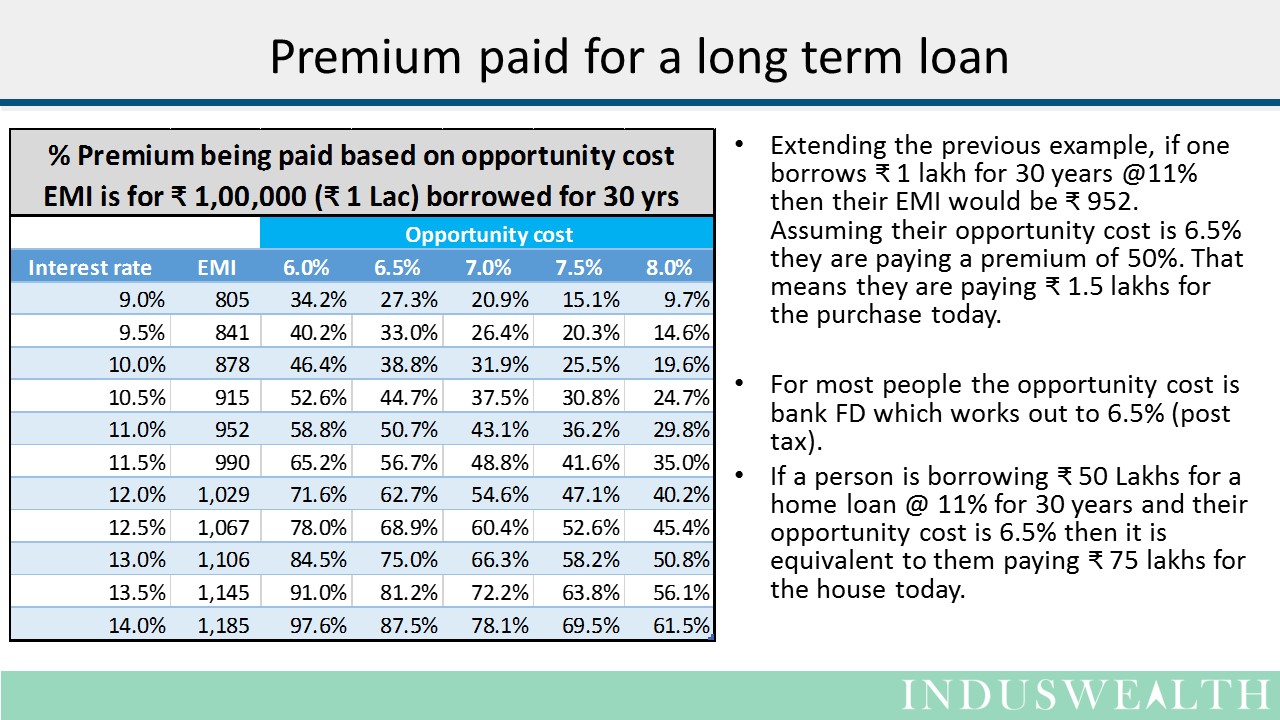

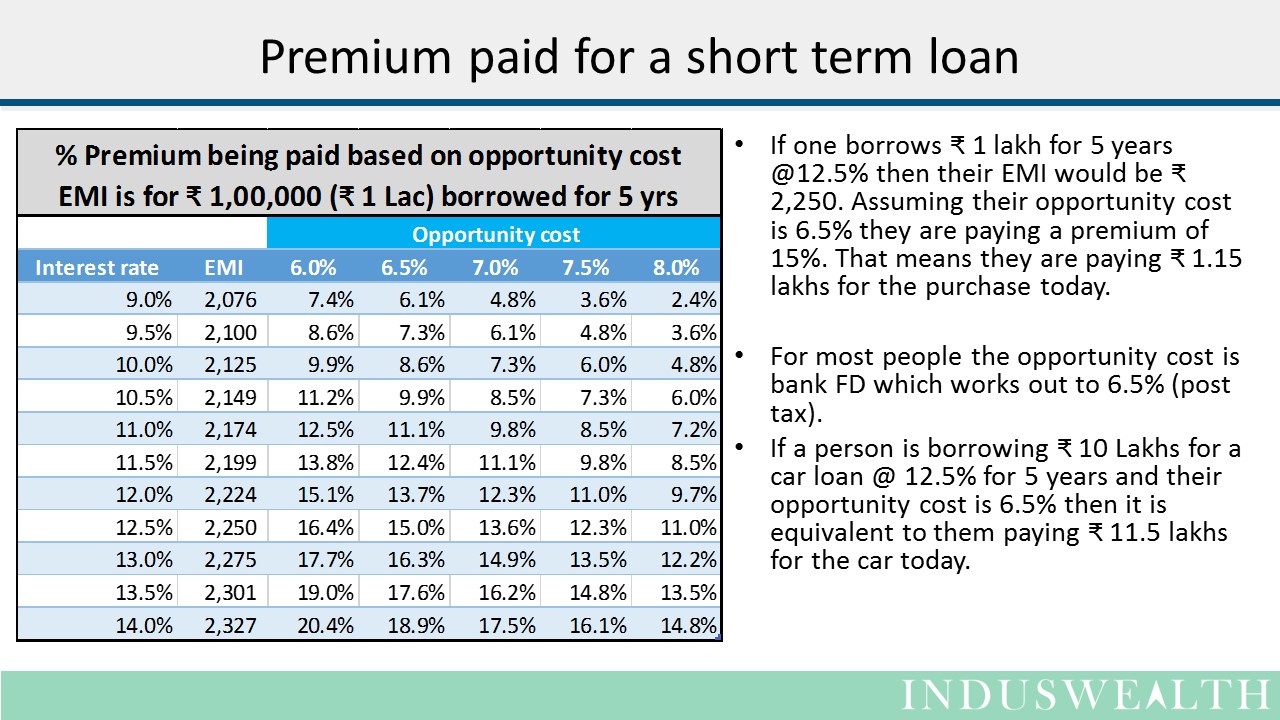

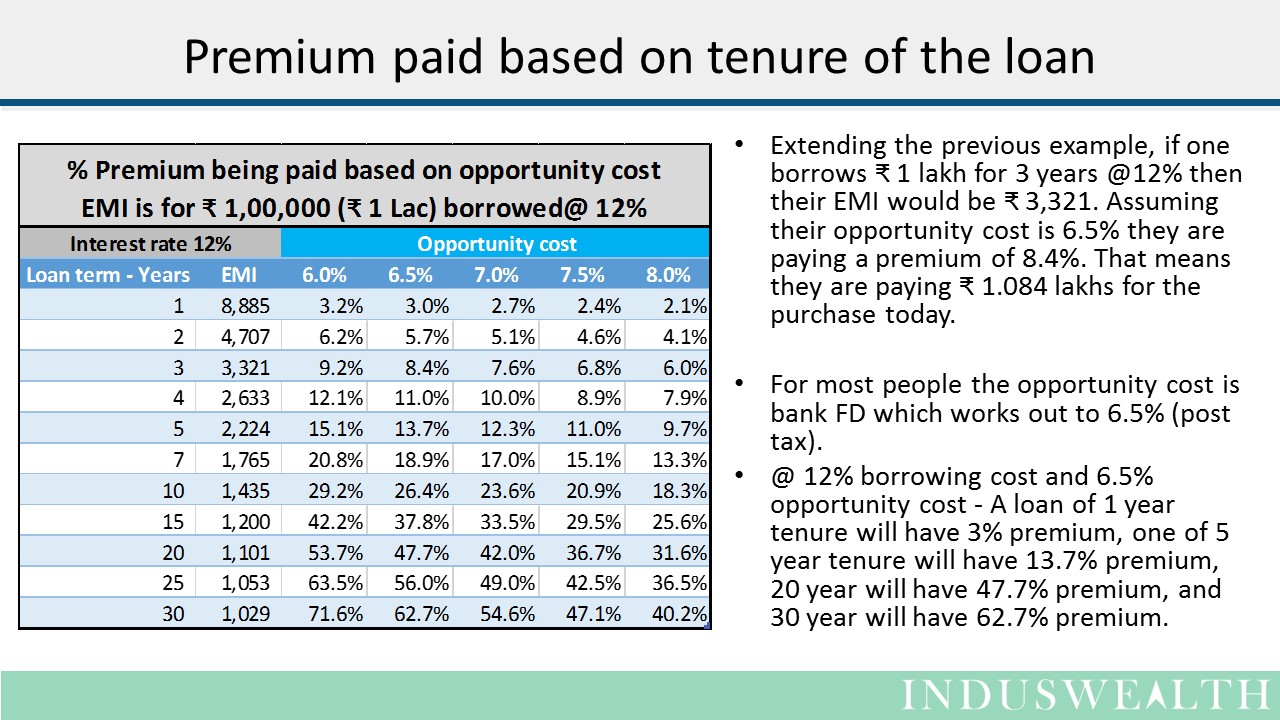

Let’s look at the premiums one pays based on their opportunity cost in real life terms:

A typical home owner who is taking a long-term loan to purchase a home is paying a premium of 30% to 50%. When home owners who take a loan calculate the appreciation of price they don’t take the premium paid into account so they get an exaggerated figure as the rate of return, thus making it look like a better investment than it actually is.

Key takeaways from this analysis:

- Borrowing makes sense when the interest rate on the loan is closer to the opportunity cost. The greater the gap between interest rate and the opportunity cost greater is the premium paid.

- If one has an investment opportunity to get a higher rate of return with a similar risk as a bank, that person can borrow at a higher rate, as the premium paid is low.

- If the opportunity cost is greater than the lending rate, it always makes sense to borrow. In this case one needs to look into the risks being taken, higher returns usually have higher risks associated with them.

- For a given opportunity cost and borrowing cost – the shorter the loan duration the smaller the premium. One can consider postponing a purchase decision and save for a while so as to pay smaller premiums.

If we think of loans in terms of the premium paid or the total cost of ownership then it will help us make more prudent decisions.

Happy investing….