I have been catching up with a few friends who have been working for a couple of decades, earning good incomes and are now considering starting their own businesses or becoming consultants in their fields of expertise.

One common theme for all of them has been that they have invested a large part of their savings in buying houses (all of them own multiple houses), they also own land, and gold. Many of their investments have appreciated well over a period of time.

The challenge they are facing is that their income may not be steady for the first 24 to 36 months while they are setting up their businesses. All of them have expenses in line with their current incomes. If they had all their wealth in a bank fixed deposit, they would be getting interest which is a few times their current expenses and they would be comfortable.

The challenge is that their assets are in real estate and gold which were not generating enough income. Rental yields from the houses are about 2.5% to 4%. For many their land does not yield any income and neither does the gold. Selling one of the houses to convert it into cash is going to take a year or so (as finding the right buyer and timing of sale are to be considered).There are also some emotions attached with selling real estate.

If we rationally look at the situation, they had above average salaries, they saved prudently and created assets – but they are still facing a dilemma as their assets are not generating enough cash to take care of their expenses.

We all would like our investments to hold their value, generate cash, and appreciate – the lacunae here is that very rarely do all these happen together.

- If an asset tends to hold its value well, it typically generates limited cash.

- Gold for instance on the long run tends to hold value, but generates no cash at all.

- Bank fixed deposits, money market instruments etc., hold their value well but they give an inflation adjusted return of 2% to 5%. With these instruments there is also a small risk of default.

- If an asset is expected to appreciate, it will typically generate very little or no cash.

- Fast growing companies, land, real estate can be some examples.

- Also the assets that can be expected to appreciate will also have a down side risk of depreciation – they usually don’t hold the value well (appreciation and depreciation are both outcomes of not holding the value).

Let’s look at the 2 features that we want from our assets

- Income generation: Safer assets tend to generate a lower income. One needs to take risk to get a higher income.

- Appreciation: Safer assets tend to hold their value better. On the other side risky assets may not hold their value well but there is a chance of appreciation (or depreciation).

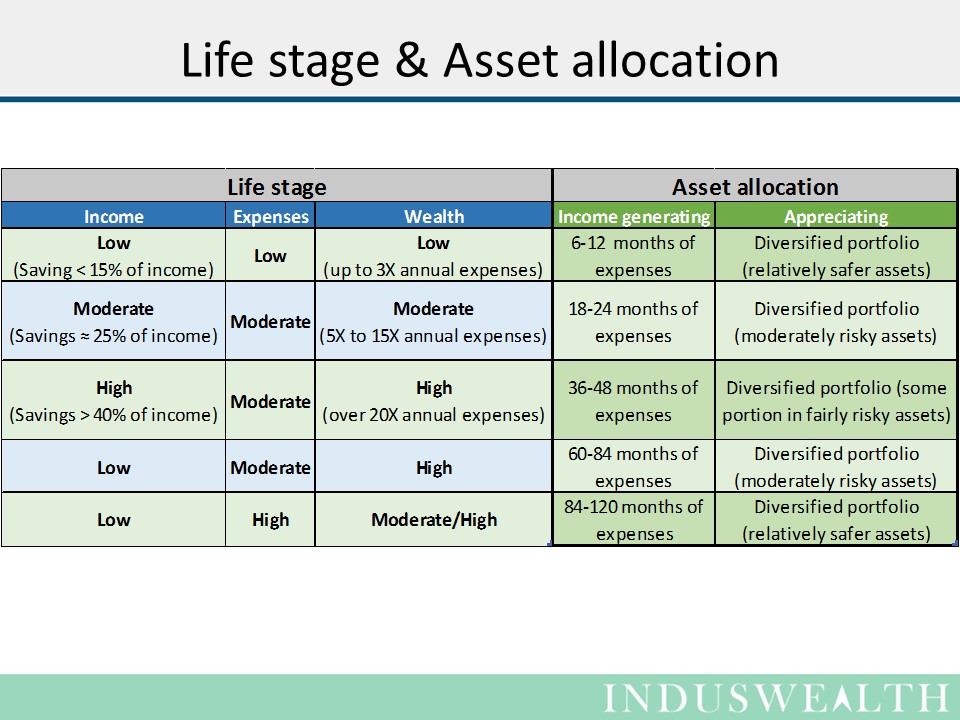

It is important that one is able to accumulate and transform assets so that they are able to cater to their current and future needs. To do this one needs to have a clear understanding of the nature of the asset – is it income generating or is it meant for capital appreciation. One has to carefully choose to find the right mix of assets to meet with their current and future needs.

Typically income generating assets should be available to address near term needs and assets that could appreciate should be there to address the long term needs. Readers may also want to refer to LEnS framework.

Happy investing…