For many buying a house is one of the most important goals. Lot of people have a significant portion of their wealth in their house. There are many reasons to buy a house – the sense of security, being able to build memories in a house where one lives, price appreciation, etc. In this article we will try and examine the economic aspects of buying vs renting a house. We firmly believe that there is no way put in a value on the emotional aspects of home purchase. We also believe that one will be able to make more informed decisions as long as they understand economics. Then each individual can make their personal trade-off’s as per their circumstance.

House purchase being a high value transaction, most will take a loan. A typical home loan is over a 20 year duration. Over the long term the interest payments typically add up to 80% to 120% of the value of the house. You can refer to the EMI calculator. Another way of looking at this is the premium paid for purchasing the house – which is usually 40% to 60% of house price at the time of purchase. You can refer to our article – Real cost of your loan.

Now let’s look at buy vs rent decision.

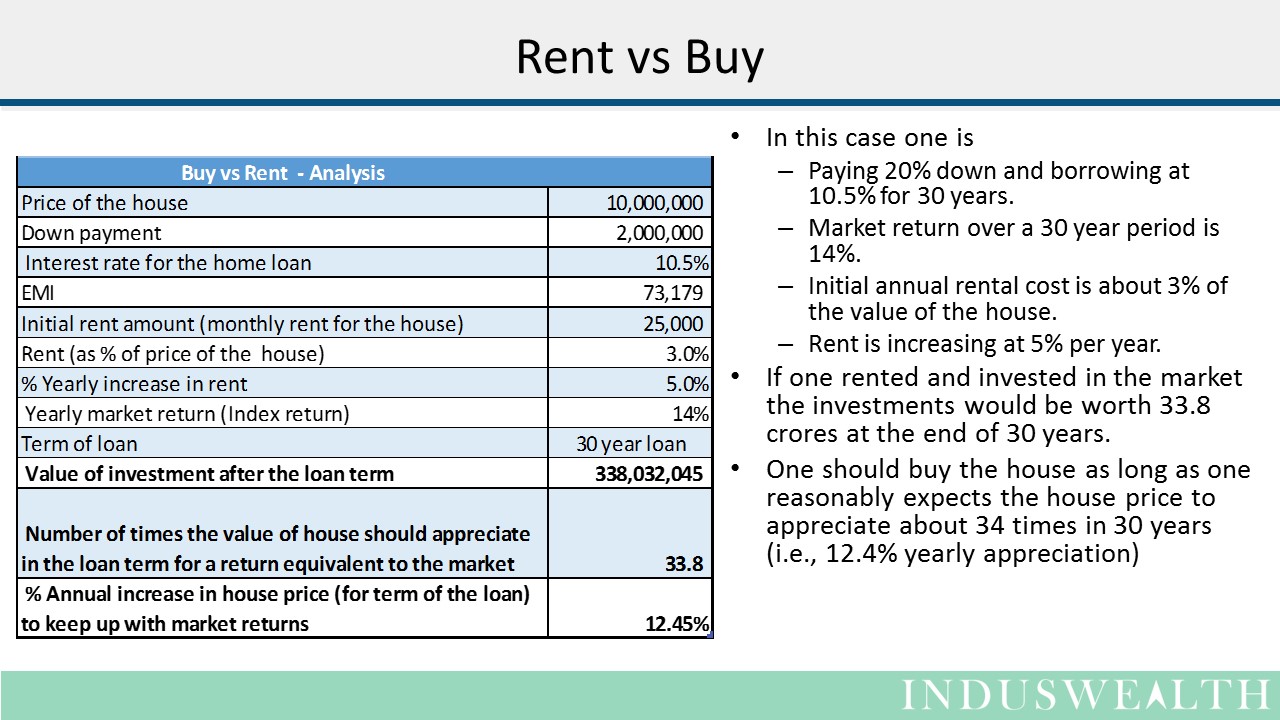

In this analysis we will look at “Borrow and Buy” a house vs “Rent and Invest” in financial products (Index fund). We will try and find out the amount of appreciation the house needs to have to provide a return similar to the financial product. You can also download “House – Buy vs Rent – DIY sheet” for your own analysis.

| Buy | Rent | |

| Monthly pay outs | EMI’s remain fairly stable, moving with the interest rates, but the changes may not be significant. EMI as a % of a person’s salary tends to decrease over a period of time. | Increases on a yearly basis.Rent as a % of a person’s salary also decreases as long as the increase in income outpaces the rent inflation. |

| Opportunity cost – down payment | Down payment made during the purchase will reduce the EMI payable. | If one is renting then this money can be invested. |

| Opportunity cost – monthly pay out | Monthly EMI’s are increasing ones equity in the house. | Usually EMI is higher than the Rent so the amount remaining after payment of rent can be invested. |

| Leverage | If the house prices appreciate then one has a significant benefit of leverage as the value of their equity increases significantly. (Equivalent downside risk also exists, albeit it has been manifested rarely, it should be taken into consideration) | Similar leverage not possible as home purchase. Home loans are usually the most inexpensive loans an individual can get. |

| Liquidity | Liquidity of house purchases is limited as finding a counter party to transact with could be time consuming. The cost of transactions are also fairly steep compared to financial transactions. | One can have a better control of liquidity of the investments by purchasing the right products. Transactions costs of financial products are usually lower. |

| Tax benefits | Governments typically encourage home ownership by providing tax breaks. The tax incentives usually reduce the cost of borrowing. | Renters also get a tax benefits, but not to the extent of the house buyers. |

| Event risks | Exposed to event risks like earth quakes, fire, Tsunami etc. | Financial portfolio is exposed to market risks, like crashes etc. |

- Expected appreciation:

- Economically one should buy a house if they believe that the appreciation they expect in the house prices is practically feasible. Best to check with historical statistics over a long run (not just a boom phase) and also compare it with the statistics in other countries.

- If the expected appreciation in house prices is lower than what is practically feasible over the long run one should rent and invest in the market.

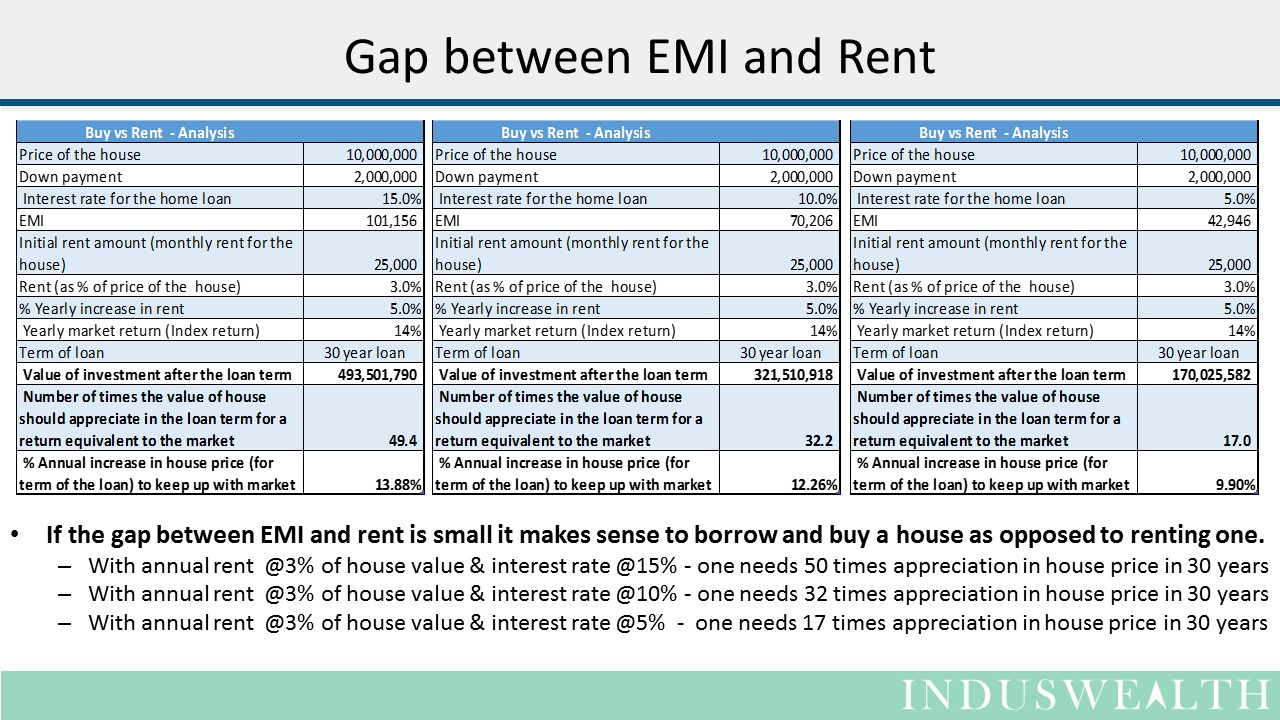

- Gap between current rent and EMI:

- If the gap between the current rent and current EMI is small then it makes sense to borrow and buy. Pl note this is a rare scenario as this will usually trigger a home building boom that will correct the scenario in a 3 to 5 year period.

- If the EMI is much larger than the current rent – then it makes sense to rent than to borrow. This means there is no demand for houses in the area and hence rents are very low. This will usually take a decade or more to correct.

- Loan tenure

- If the loan tenure is short then it is better it is to borrow and buy

- If the loan tenure is long then it is better to rent and invest

This means ability to pay back the loan quickly is important.

- Down payment:

- All other things remaining same – % down payment itself has limited impact on the appreciation of the house price required to match market return.

- Higher down payment can translate to lower EMI and hence shorter tenure – thus its impact can be indirect.

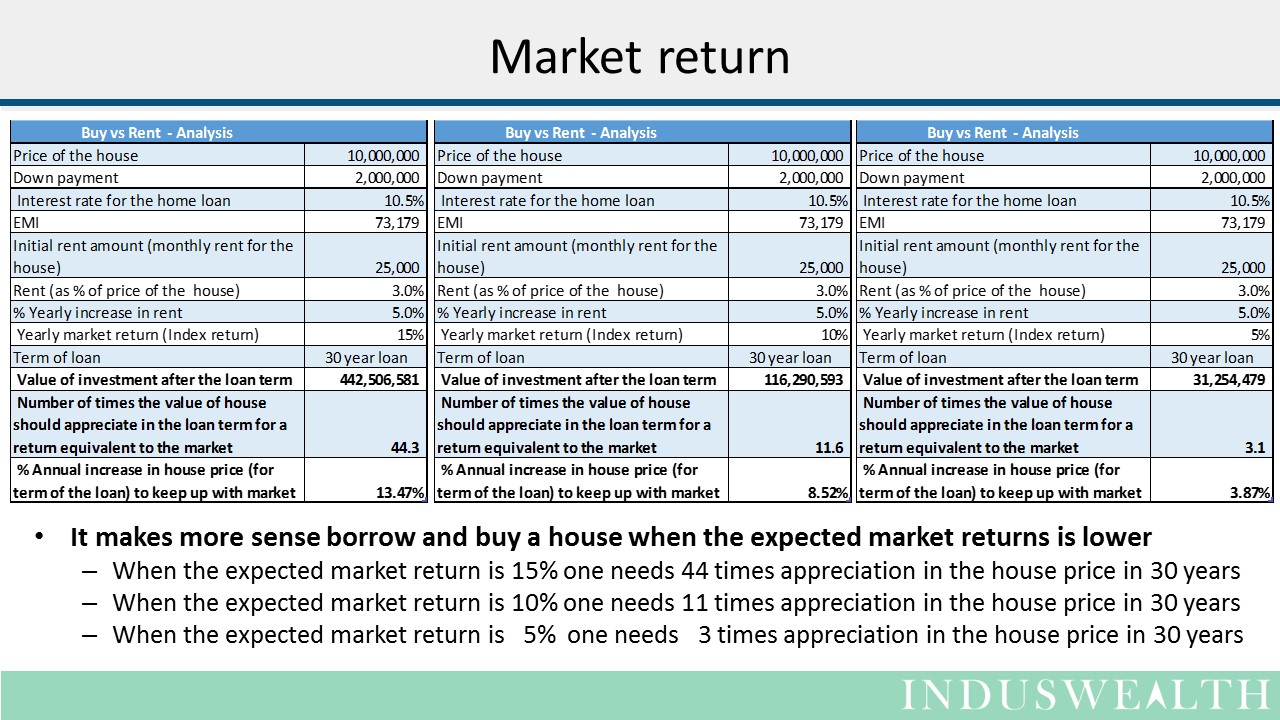

- Expected market return:

- If the expected market return is low – It is better to borrow and buy.

- If the expected market return is high – It is better to rent and invest.

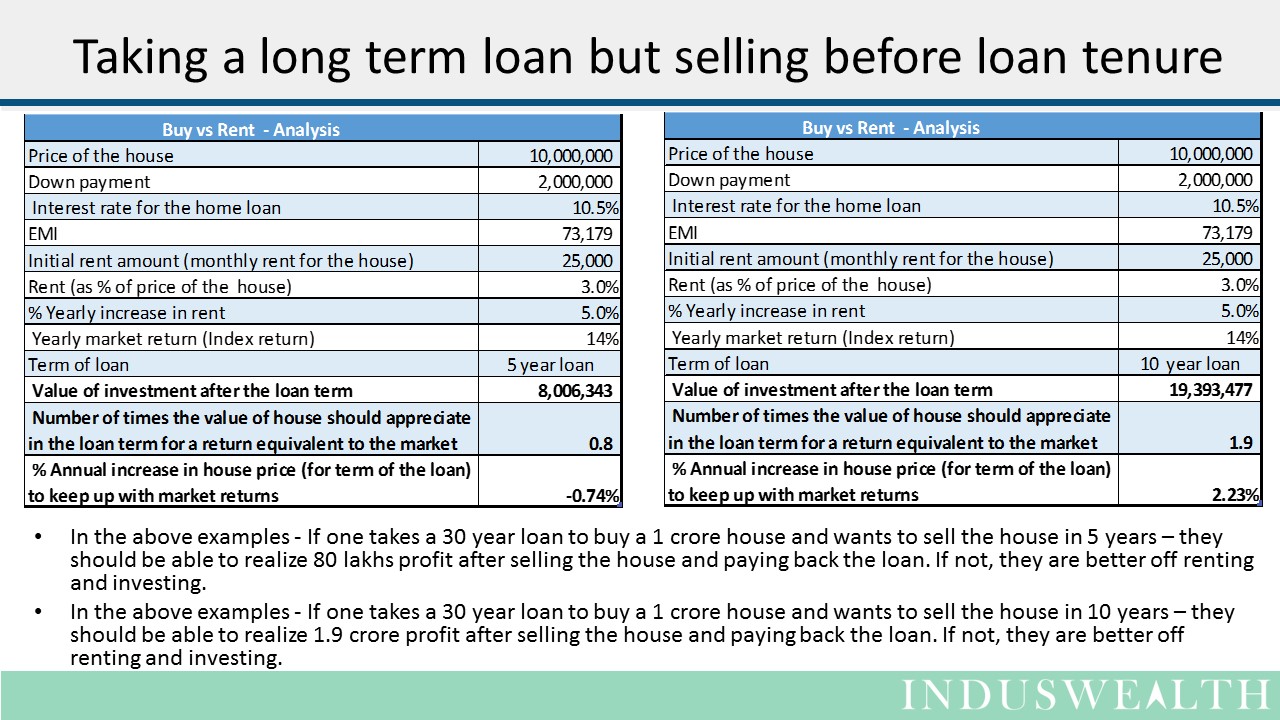

- Taking a long term loan but selling before the loan tenure

- Here one should look at the potential sale value of the house vs the value of investments if one rented and invested to figure out if the trade-off is profitable. (In the DIY sheet one can use the drop down for a lower loan and input the actual EMI being paid)

- Liquidity: Home buyers should be ready for limited liquidity as closing house transactions can be time consuming. They need to have alternate plans to manage their liquidity.

- Insurance: Home owners are best advised to purchase catastrophe insurance to hedge against extreme events (fire, earth quakes, tsunami’s etc).

- Diversification: One should try and ensure that their house (investments in real estate) does not represent more than 40% to 50% of their wealth.

In summary we can say that house purchase is a fairly complex choice even when we use just the objective criteria. The subjective and emotional criteria make it even more challenging task. We hope this analysis and the DIY spreadsheet gives you some tools to analyse your house purchase.

Happy investing….