Our recent article House – Buy vs Rent received a very good response and one of the often asked questions was “when should one buy a house?”. In this article we will explore the decision to Buy now or Wait.

Let’s look at a story of 2 friends who have very similar profiles – Harish and Pavan – both are about 25 years old and have very similar jobs and expenses. Harish is in a hurry to be home owner and Pavan is ready to be patient. Both of them would like to live in a house that costs about Rs 1 crore.

A 30 year loan is available at 10% interest. A similar house can be rented at 3% of the cost of the house which works out to RS 25,000 per month. Rents are reasonably expected to increase at 5% per year.

Harish was able to find a bank which was ready to give Rs 1 crore loan at 10% interest with zero down payment and EMI was Rs 87,757. EMI would account for a bulk of Harish’s salary. He reckoned that as he went along his salary would increase and the EMI as a percentage of his income will become smaller. He was also going to save the money on rents and get a tax break on the interest.

Let’s look at how what Harish’s money is getting him:

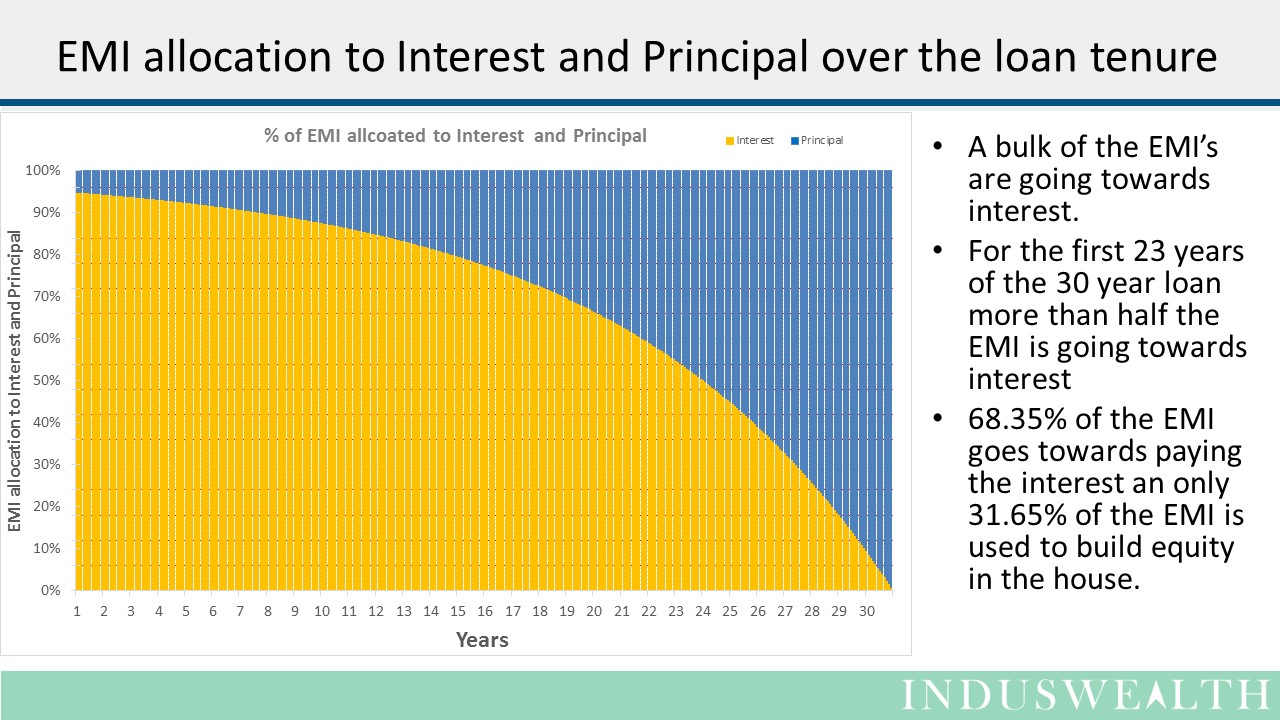

68% of the total money paid by Harish was going towards interest.

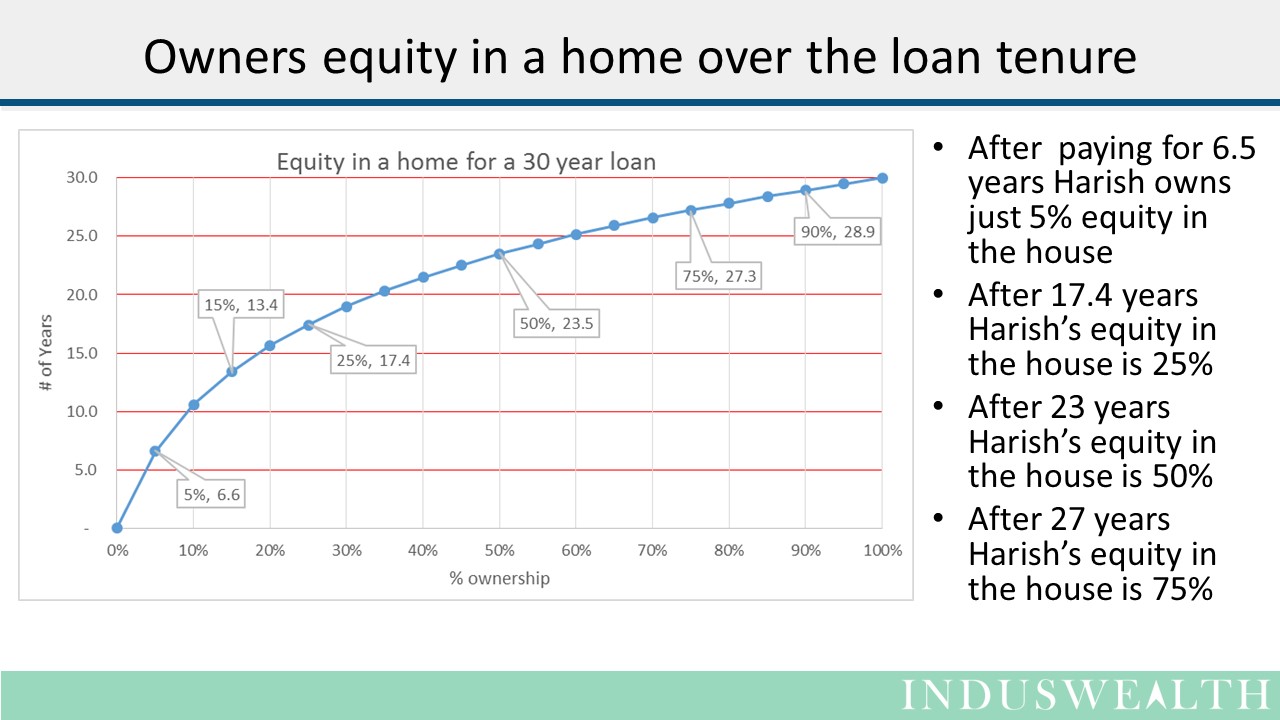

Harish’s equity is the house is 50% only after 23 years i.e, after 75% of the loan duration.

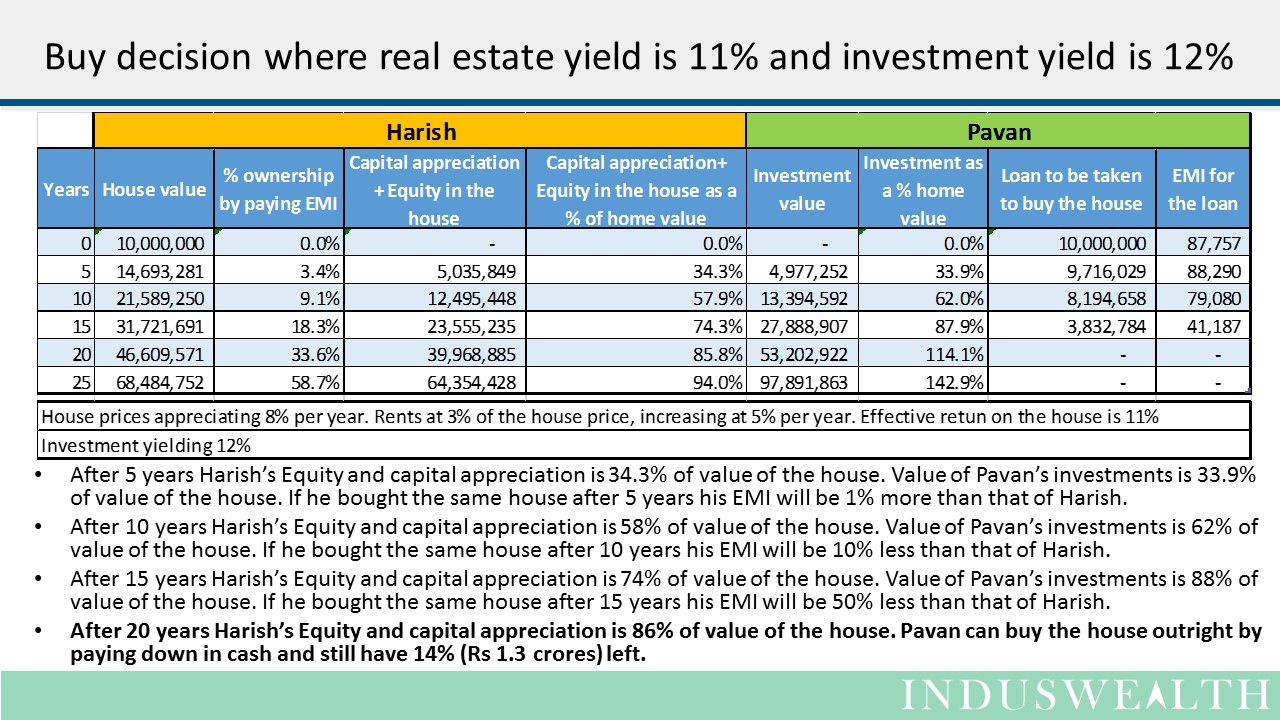

Pavan felt that buying a home at a very early stage in his career might put him under significant financial stress. He decided to rent a similar home and invest the difference between the EMI and the rent in an Index fund. Pavan did a bit of research to find out the NIFTY was giving a return of 15% annually for long term investors. He also checked other developed markets and realized that US and UK markets have given 10% returns for over 60 years. Being conservative, Pavan assumed that he is going to get 12% return on his investments. He also assumed that the home prices will increase at 8% per annum, while generating/saving 3% per year in rents – so giving a net yield of 11% per year. He did some quick numbers.

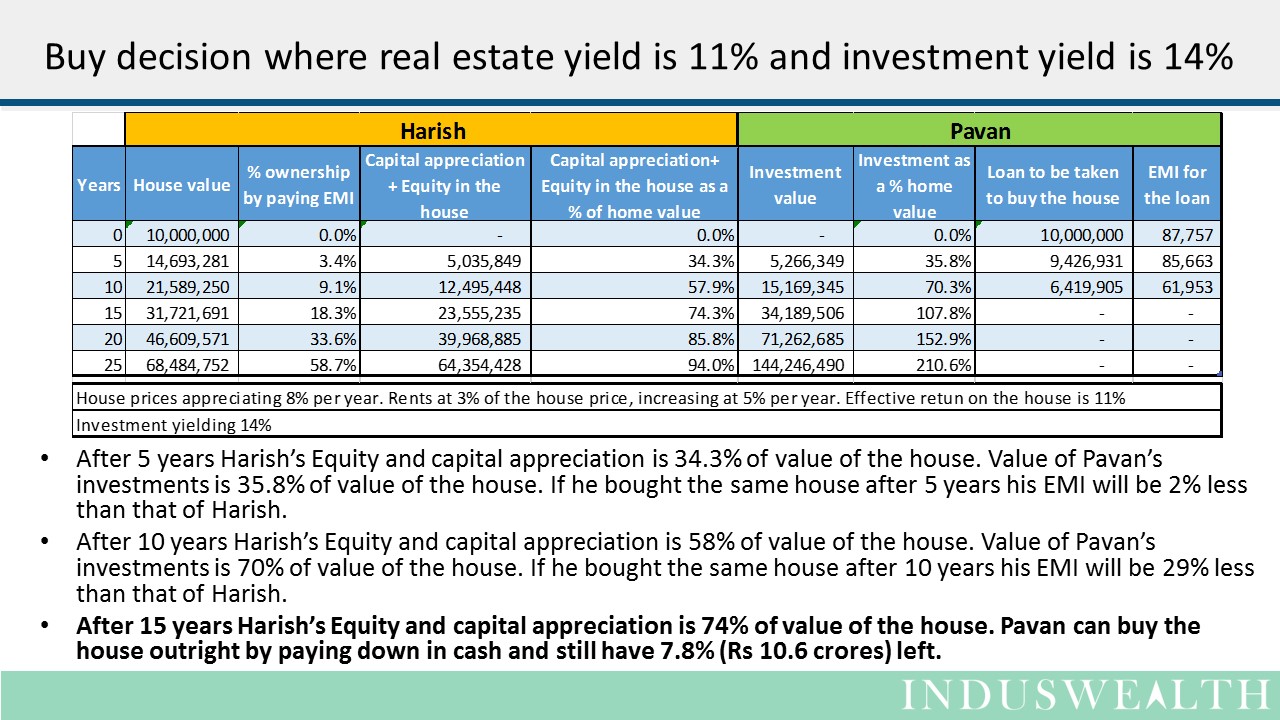

With an investment return of 12% per annum. Pavan is better off waiting for 15 years or more to buy the house.

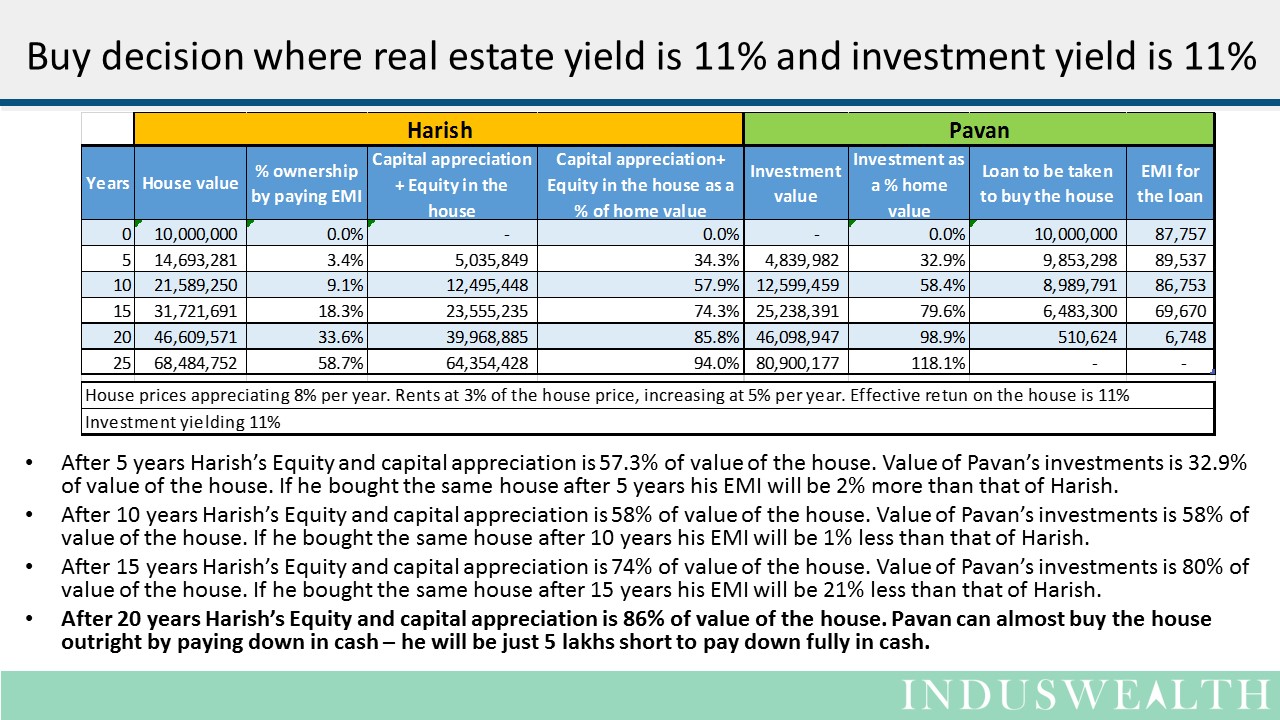

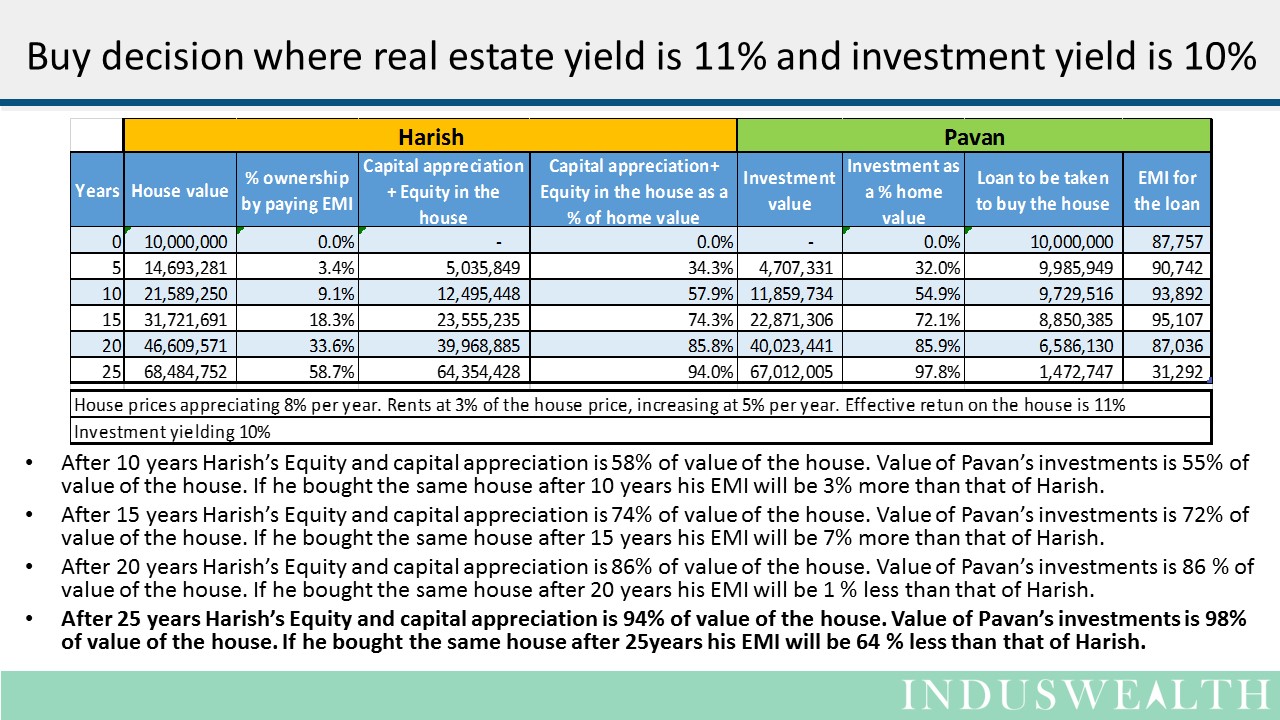

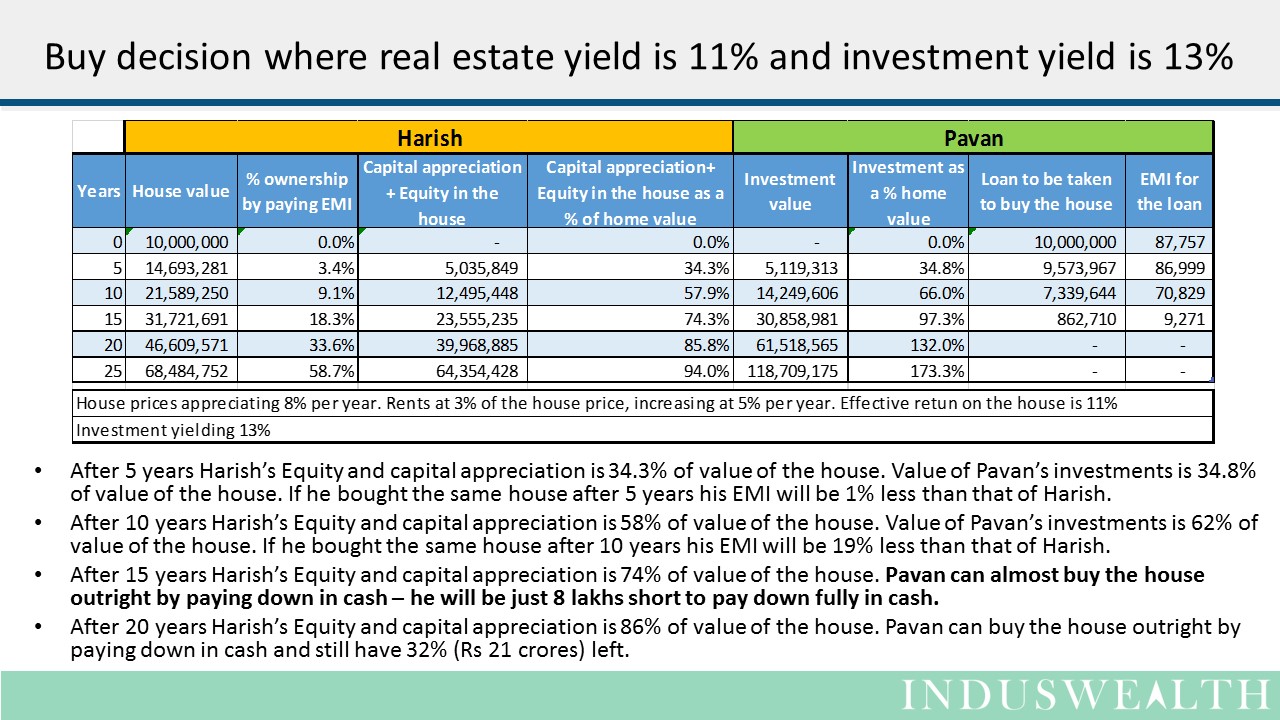

Let’s look at couple of more scenarios where the return on the investment is different…

In a case where markets (Index) and real estate are giving similar returns it makes sense to wait for more than 15 years.

In the case where markets returns are lagging real-estate returns one needs to wait a bit longer. This is particularly rare scenario as markets and real-estate both represent wealth. Historically market returns have been better than real-estate returns.

Based on the scenarios presented here – financially it is always better to delay the purchase of a house and use that time to build a corpus to for the down payment.

One thing most people don’t realize is that home purchase is a large play on leverage – if the home price actually falls (yes this has happened in places – best example being the 2008 crisis) or stays flat (current scenario in Indian market) – then the person taking the loan is taking a huge risk. When one takes a loan bulk of the future earnings are going towards paying interest to the bank rather than building one’s wealth.

Purchase of a house at an early stage of one’s career makes the person less mobile – as home owners generally tend to be a bit less geographically mobile. Also there are huge transaction costs (both in terms of money and time) involved in closing out a house transaction. There are also risks of job uncertainty or opportunities to be an entrepreneur – that a person with a large EMI may find challenging.

An investment (including the purchase of house) can be called “as safe as a house” only when you own most of it – not the bank (or a lender).

In summary we can say that home buyers are usually better of building up a corpus before buying a house. We believe that people who are starting to earn should invest in Index funds for the first 15 years and then think about purchasing the house.

With people living longer and retiring later – purchasing a house at age of 35 to 45 may help people make better choices and still have a lot of time to enjoy their investment without the worry of paying the lenders.

We hope this article answers some of the questions raised and gives clarity to your investment decisions.

Click here to download a DIY sheet to do your own analysis.

Happy investing….