* This is an English version of the article published by us in Vikatan magazine. (download article)

We believe this is a path setting budget rather than a path breaking budget. Ideally, governments should be in the business of setting policy based on its priorities and providing a stable environment. Private enterprise should be should be looking to leverage opportunities to provide goods and services and generate value for its stakeholders. This budget is furthering the maturing of Indian economy by making many path setting announcements.

What we like about this budget is that it provides direction to the industry by stating the intentions of the government upfront for the next few years (for instance Corporate tax) and laying down specifics about the near term (deferring of GAAR). These measures definitely give confidence to the industry that they will be operating in a more stable policy environment thus encouraging further investments. We believe that it will take a further 12 to 18 months to see a tangible uptick in the investments and may be 24 to 30 months for the large projects to become operational. Investors should look to build up their exposure to equity over the next few years to be in a position to benefit from the uptick in the economy. We also advice against rushing into investing “right now” as we believe markets always have opportunities for prudent investors. The policies of this budget create a long term path for prosperity and investors can steadily build their portfolios through regular investments.

REIT’s– establishment of real estate investment trusts is a positive step both for the firms that have significant real estate assets and individual investors. This allows real-estate firms to monetize their assets and thus help them improve their liquidity and enable them to finish projects or take up new ones. REIT’s enable individual investors to have an exposure to real estate sector in a more flexible way as they can buy and sell them like shares thus improving the liquidity of their real estate holdings. We believe that due to overcapacity in the housing sector which has an inventory of over 1.5 lakh units, lots of unfinished projects in pipe line and muted demand it make take a couple of years for this sector to revive. We advise investors to build up their exposure to REIT’s as they become available. We also advise them to exercise caution while taking direct exposure to firms that are into real estate development as we believe it will take some time for them to get into a decent shape.

Gold monetization: India represents 3% of world wealth but over 12% of world gold. Indians appetite to buy and hold gold means that a significant part of the assets in India were not available for wealth creation. Announcements about providing gold bonds and also opportunities to deposit gold will help deploy it for wealth creation. We believe overcoming cultural inertia and making this operational will take about 5-10 years. This policy might create an environment where prices of gold may tend to be stable for a long time and may witness any significant appreciation. We advise people holding gold as an investment to leverage gold bonds and deposits, as this reduces the cost of holding gold and provides income. We advise our clients to limit their exposure to gold to a maximum of 10% of their total assets.

Social Security: We really appreciate and welcome the steps taken by the government for setting up of social security – this will enable poor to invest for pension as well as have death and disability insurance. Our analysis indicates that the insurance premiums that people have to pay are very pragmatic, thus providing a good cover for the citizens without creating a significant burden on the national finances. We advise readers to encourage their domestic help, drivers, and others who can benefit from the social security plans to take active steps to participate in these. We also advise people who are closer to retirement to take advantage of the tax benefits of Rs 50,000 and invest in the pension scheme. Individuals whose retirement is more than 10 years away might be better off considering equities as the vehicle for savings. We advise all the readers to leverage the increase in Health insurance cap from 15,000 to 25,000.

What we would have liked to see in the budget:

- We would have liked the government to enable PPF to invest its funds in equities, as equities tend to generate a better rate of return for longer term horizon. Current PPF investments are all in debt products, which may not be suitable vehicles for retirement planning.

- We would have liked the government to nudge players to offer low cost Index funds as ELSS schemes. Currently there are no low cost Index funds available as a part of the ELSS, so the investors are paying high fees thus reducing their long term returns.

In summary, we like the current budget but believe that execution of the stated policies and passing of key bills like the land acquisition bill to be critical for the long term success. Budgets should be boring events, in developed countries budgets do not get this kind of attention, we believe that this government has taken the first step towards making budgets boring non-events. We wish them all the success in accomplishing it.

Views on the investment and the investment environment

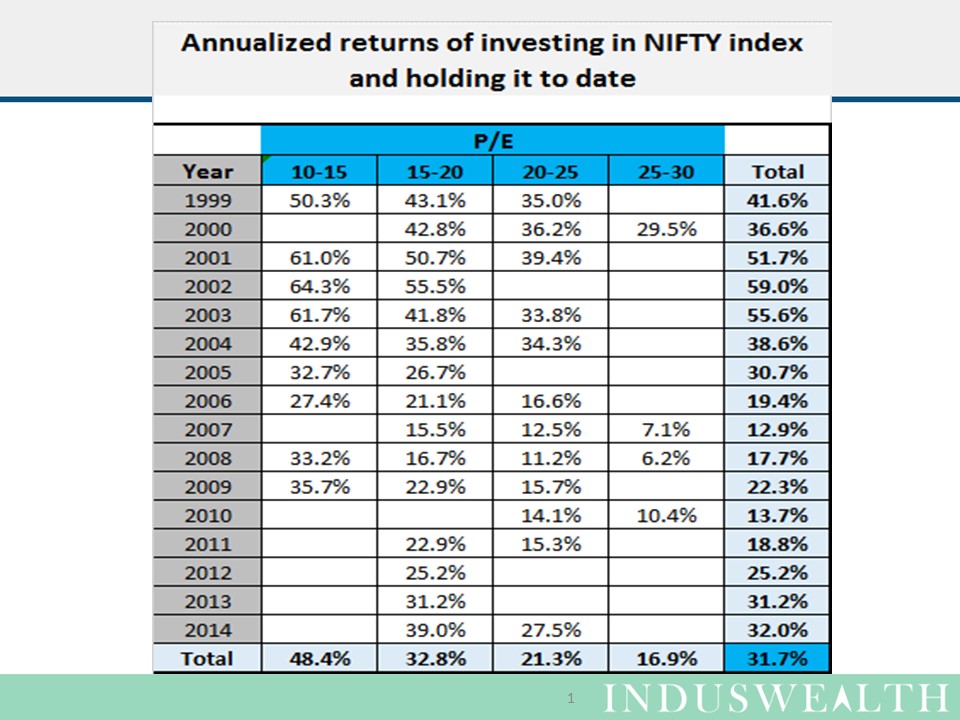

An excellent business could be a poor investment if bought at a high price, similarly a modest business could be a great investment if purchased at the right price. Purchasing at the right valuation is the key to investment success. We believe that P/E is one of the best indicators of a firm’s valuation.

Let’s look at the annualized returns from investing in NIFTY on from 1999 and holding them to date:

- If one purchased NIFTY index in 1999 and held to date

- 1 lakh invested when the P/E was in the range of 10-15 becomes 9 lakhs (800% return, 50% per annum)

- 1 lakh invested when the P/E was in the range of 20-25 becomes 6.4 lakhs (540% return, 35% per annum)

- Investing when the P/E is low generates 2.6 lakhs (40%) more

- If one purchased NIFTY index in 2008 and held to date

- 1 lakh invested when the P/E was in the range of 10-15 becomes 3 lakhs (200% return, 33% per annum)

- 1 lakh invested when the P/E was in the range of 25-30 becomes 1.44 lakhs (44.5% return, 6.2% per annum which is just less than the bank rate after taxes)

- Investing when the P/E is low generates 1.56 lakhs (100%) more

- Perspective for investors

- Valuation (P/E) at the time of investing makes a significant difference to the returns, best to invest when the P/E’s are lower

- The longer one holds onto the investments the better the returns (this is due to the power of compounding and long-term northward bias of the markets).

Current P/E levels in the market is about 23.5 and this is fairly high, we still believe that there is still a case to be made for investing in equities.

- Reasons for investing in equities

- Market cap to GDP ratio of India is about 0.8 and that of developed economies is well above 1, that means

- As India’s GDP is expected to grow at 8% to 10%, so the market cap can be reasonably expected to grow at the same rate (assuming the ratio does not change)

- There is a room for correction of the GDP to Market capitalization ratio from 0.8 to 1, this creates a room for further 25% upside. We believe it will take 5 to 10 years for such a correction, this means one can factor in 2.5% to 4% upside on annualized basis.

- Increase in depth of the market:

- Retail participation in the Indian markets is less than 10% of the total market capitalization. We expect more retail participation in equities as the levels of awareness rise as well as alternate opportunities (real estate and gold) become less attractive. This increase in depth will lead to more stable prices (as this will counter balance FII’s), and also may lead to 2 to 3% increase in prices.

- Global environment is positive with a recovery in US, Japan and Europe are also looking more stable. A dynamic business environment and government in India can make India seem more attractive compared to Brazil and China, thus resulting in sustenance of FII funds and also attracting capital for investments. This might lead to another 2 to 3% upside.

- Market cap to GDP ratio of India is about 0.8 and that of developed economies is well above 1, that means

- Concerns for investing in equities

- The current P/E of 23.5 is very high thus adding to the risk. This can be mitigated only if the there is a sustained increase in earnings reported.

- Oil prices can be reasonably expected to increase from these levels. Even though the prices have been linked to the market, a steep increase in Oil price will have an impact on the fiscal deficit and government policy.

- QE (Quantitative Easing) and response to sustained austerity in European counties (like Greece and Italy) can bring in a certain amount of lack of stability.

Considering all the factors, investors can expect 12% to 15% annual returns if their investment horizon is 3 to 5 years. We advise our clients to invest funds which are available for long term investment (at least 3 to 5 year horizon) in equities. We suggest a buy and hold strategy as this will help them take advantage of the tax breaks available for long term capital gains in equities.

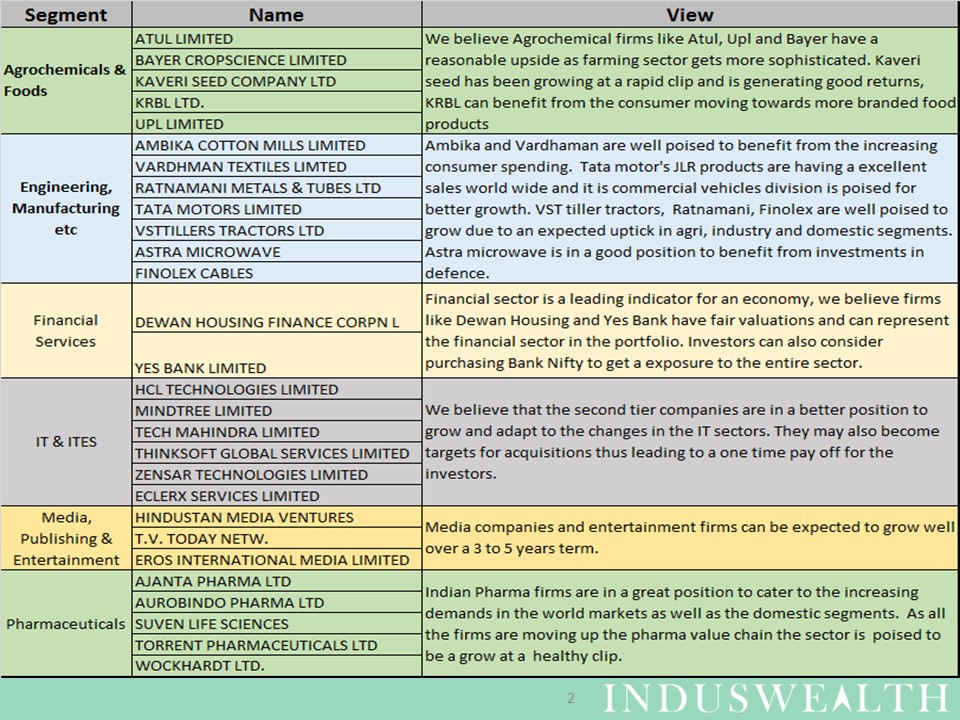

Stocks that can be considered for investments

- Based on our analysis we believe that the following stocks can be considered for investing

- We advise investing in a diversified portfolio of stocks, we suggest that one should not invest more than 5% in any individual stock.

- People who do not have the appetite to invest in direct equities can consider investing in Index funds. We suggest investing 70% of funds in NITFY and 30% in Bank NIFTY.

We suggest to the readers that equities should constitute at least 20% of their total wealth. If people have less than 20% exposure they can build this by buying equities regularly over 18 to 36 months.

Pl remember investing is a journey, selecting the right investment products, having discipline and patience are key to investment success. Also people who do not have an appetite to absorb a 10% to 15% downside should desist from investing in equities.

Happy investing..