When a kid is asked to choose between 2 toys, the kid is trying to figure out which gives her greater pleasure (value). As the kid grows up the she has to continue to value various options – which profession to pursue, which career to choose, which city to live it, who and when to get married etc. All of these choices are fairly tough to evaluate and some more so than others.

We believe valuing investment options is relatively easy as they have fewer subjective dimensions and the frameworks to evaluate these are available.

In simple terms, all financial products are transformers – they transform current money into future money (deposit products) or future money into current money (loan products).

Valuation of financial products is about valuing of money over time – for instance

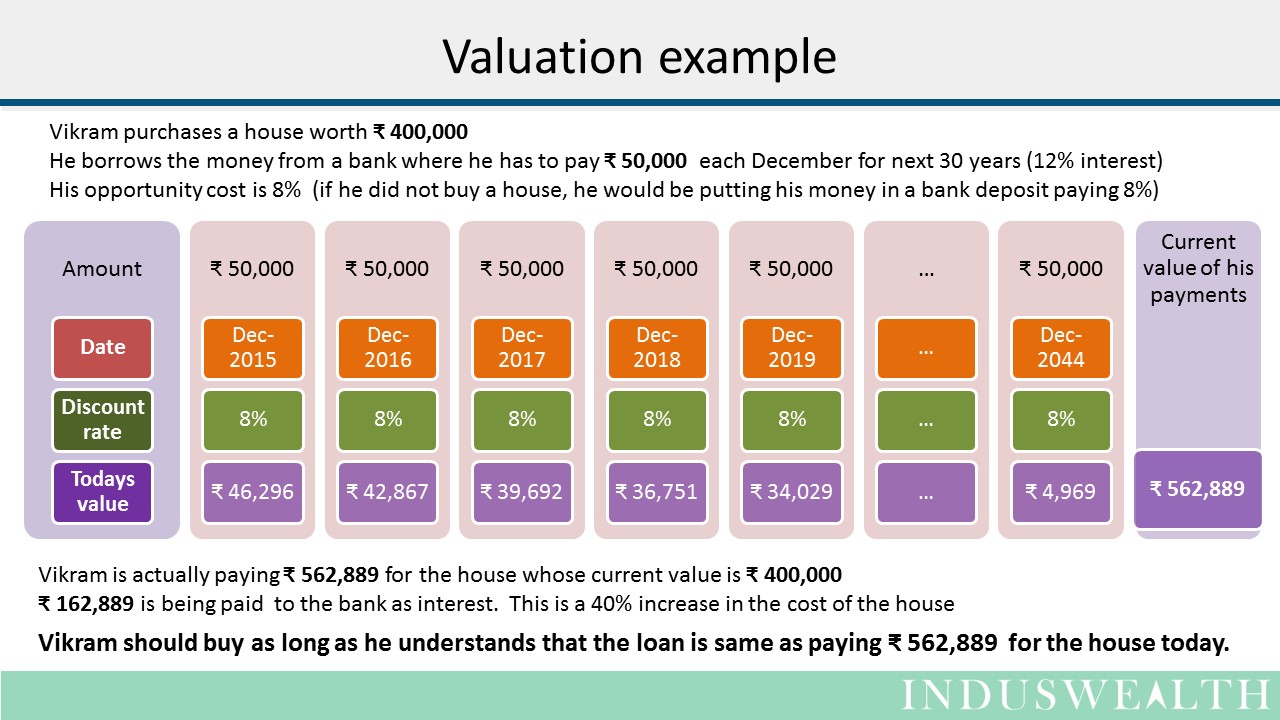

- If one is buying a house with a 30 year loan – one is evaluating the benefits of the house that one will enjoy vs the EMI one will be paying for next 30 years. Here future income is transforming into home ownership today.

- If one is saving to buy a car by giving up current consumption, one is valuing the benefits of the car ownership later vs the gratification from spending the money. Current income is transforming into a car ownership later.

For most of the common products (deposit, loan, insurance, etc.,) this valuation is relatively straight forward as long as one has a good idea about the 3 W’s

- What are you paying or getting – clarity about the amounts one is going to pay or receive

- When are you paying or getting – clarity about when the payments or receipts will

- What does it cost – this is evaluating what money today is worth later or vice versa. Here one would be using the principles of compounding. The rate to be used for compounding (a.k.a. discount rate or opportunity cost) is a bit subjective, but one can identify “reasonable” guidelines to follow.

- A person with limited risk appetite one should look at the bank FD rate

- A person with an appetite for equities one should look at the long term Index returns

- A person running a business should use the rate of return from the business that is expected in the long run

Once one has a clear idea of the 3W’s all one has to do is list down all the cash flows on a timeline and then discount them to current date.

Let’s look at an example:

Pl remember financial valuation of something can only indicate what it costs – what it is worth to someone is very subjective and individual specific.

Happy investing….